Are your property taxes going up? NJ pension costs rise 9%

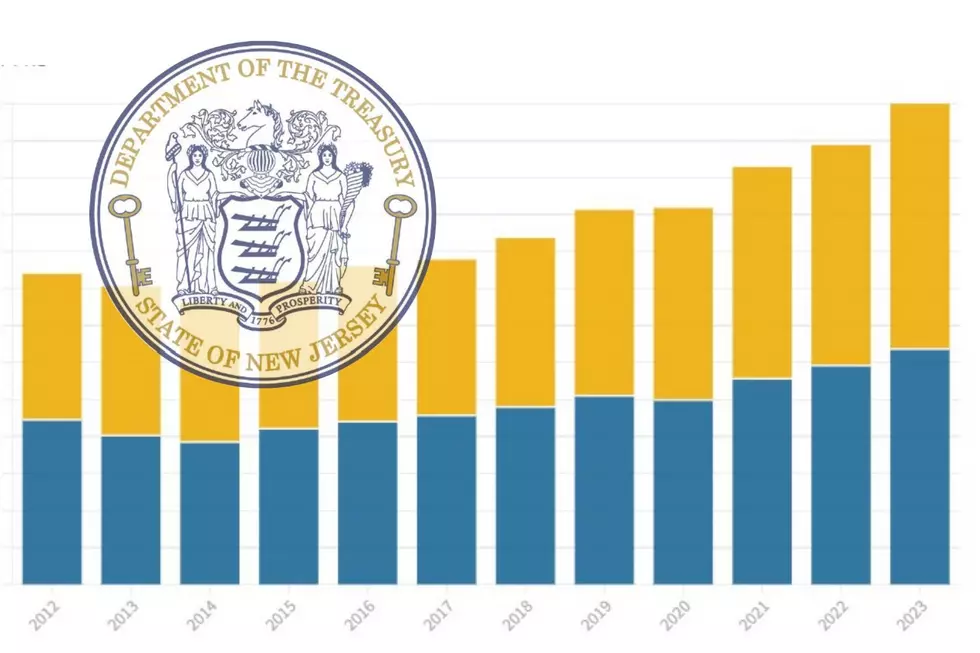

TRENTON – New Jersey local governments in 2023 will be paying the biggest increase in pension costs since reforms to public workers’ benefits made more than a decade ago, according to bills sent last week that further ramp up pressure on property taxes.

Local government contributions to the Public Employees’ Retirement System and the Police and Firemen’s Retirement System will be just under $2.6 billion combined, an increase of almost $224 million, or 9.4%, from what they paid this year.

That is slightly more than the $222 million increase in 2021 and follows a $118 million increase this year.

Lots of costs are going up for municipalities

Michael Cerra, executive director of the New Jersey State League of Municipalities, said the pension bill isn’t shocking but that coupled with a big jump in health care costs, as well as inflation, it’s going to have a significant impact on local budgets in 2023.

“What is catching everyone’s eye is that it’s simultaneous with other very significant increases which sort of all come from the same source eventually, which is the property taxpayer,” Cerra said.

“It’s really just sort of a piling-on effect here – that it’s not just one thing, it’s multiple,” he said.

What about the property tax cap?

Increases in costs for pensions and health benefits are exempted from the 2% cap on increases in property tax levies. With local governments likely to need all that cap space to deal with inflationary pressure on their costs, it’s more likely to mean larger-than-usual property tax hikes.

“No local official wants to add this to the property tax,” Cerra said. “But these costs have to be paid somehow.”

There’s no official price tag on the higher costs for health benefits, but it could be over $350 million.

Actuaries determine the pension contribution rate, based on worker salaries. Rates come to 36.51% of the salary of cops and firefighters, up from 33.25% this year, and 17.11% of the salary of other local workers, up from 15.98%.

Next year is also the last of a three-year phase-in of the results of a statutorily required experience study by plan actuaries.

“Annual costs typically grow year over year, because they are based on an actuarially determined contribution rate applied against the pensionable salary of each employee,” said Treasury Department spokeswoman Danielle Currie. “If pensionable salaries increase, then the employer’s pension cost will increase accordingly. The appropriate and accurate way to evaluate year-over-year cost increases is on a percentage basis.”

It’s also affected by the state reducing its assumption for how much its investments will increase in value in the future – which is more fiscally responsible but pushes up contributions as a result. Then-Gov. Chris Christie lowered the assumed rate of return from 7.65% to 7% in his last month in office, but the Murphy administration revised that to phase in more slowly over five years.

“This year’s increase is also driven by the impact of the reduction in the pension fund’s assumed rate of return from 7.3% to 7% to bring it in line with long-term expectations without completely overburdening local employers,” Currie said.

Is the state paying its share?

The state government is making the full contribution to the pension funds recommended by actuaries, around $6.8 billion, for the second consecutive year. But it will be years before those payments lead to budget relief, after a quarter-century of shorted payments.

Of the $2.6 billion that local governments must pay toward pensions in 2023, $604 million is the regular current cost for the pensions – and more than $1.86 billion goes toward the unfunded liability.

John Donnadio, executive director of the New Jersey Association of Counties, said local governments have been making full contributions for a long time but are suffering in part due to longstanding fiscal mismanagement by the state.

“Although the annual increases may, in part, be explained by underperforming investments, a reduction in the assumed rate of return for long-term investments and other relevant factors, NJAC contends that the state continues to use local property taxpayer dollars to subsidize the massive unfunded accrued liability it created,” Donnadio said.

Currie said that statement is inaccurate and that local employer contributions are not used to help fund the unfunded liability of the state component of the plans. Actuaries calculate the state's contribution using revenues and expenses for the state plan and separately calculate local contributions using financial details for the local plans, she said.

"There is no cross-subsidization between the state and local components of the plans," Currie said.

How much more will my municipality pay?

The percentage increases vary by local government. You can look up the increased pension costs for your counties, towns and school districts through the reports accessible through the following links:

Public Employees’ Retirement System: 2023 bills, detailed … comparisons to 2022

Police and Firemen’s Retirement System: 2023 bills, detailed … comparisons to 2022

Michael Symons is the Statehouse bureau chief for New Jersey 101.5. You can reach him at michael.symons@townsquaremedia.com

Click here to contact an editor about feedback or a correction for this story.

2021 NJ property taxes: See how your town compares

How is it still standing? Look inside the oldest home for sale in NJ

More From New Jersey 101.5 FM